Fix housing to improve aged care budget

What does housing have to do with the blow out of the aged care budget? A lot, actually.

Older people want to stay at home as they age, with many wanting to stay in the home they have lived in most of their lives.

However, the reality is that many homes built throughout the 20th century are not well suited to older people living alone who may be experiencing age-related changes in mobility, health, and independence.

Yes, we can modify homes to be more age-friendly, but that comes at a cost and doesn’t address the other elephant in the room: the ongoing cost of maintaining a home.

The entry-level Commonwealth Home Support Program (CHSP) and the higher-level Support at Home programs provide funding to support someone to maintain their home, to keep them out of residential care.

Billions of dollars are spent on subsidies for gardening and cleaning in recognition that these activities get harder as you get older. Fair enough.

Between CHSP and Home Care we spend about $4.4 billion (28% of total spending) on cleaning and home maintenance activities. Funding for home modifications is also available, but the annual cost of the new scheme isn’t public knowledge.

But is this the best and most cost-effective way to support ageing in place? Surely, these year-to-year costs would be less if people were in smaller age-friendly homes; but these homes do not exist.

No one is suggesting that we force people to downsize their home, absolutely not! But for those who might want to downsize, the options are limited. Why?

Keep reading to complete our reader poll at the end of this article.

The housing market has failed older people too

Almost every day in the media is another story about the failure of the housing market. Young people are increasingly locked out of a market and seniors are partly blamed.

Yet there is little said about the failure of the market for seniors.

While most older people are lucky enough to have homes, many don’t have options to change their housing, even if they want to.

NSA research shows that about one-third of older people are considering downsizing but face a myriad of barriers, with the availability of appropriate homes just one of these.

Seniors friendly housing is limited, unattractive, or focused on people with wealth.

It’s a problem with the whole market.

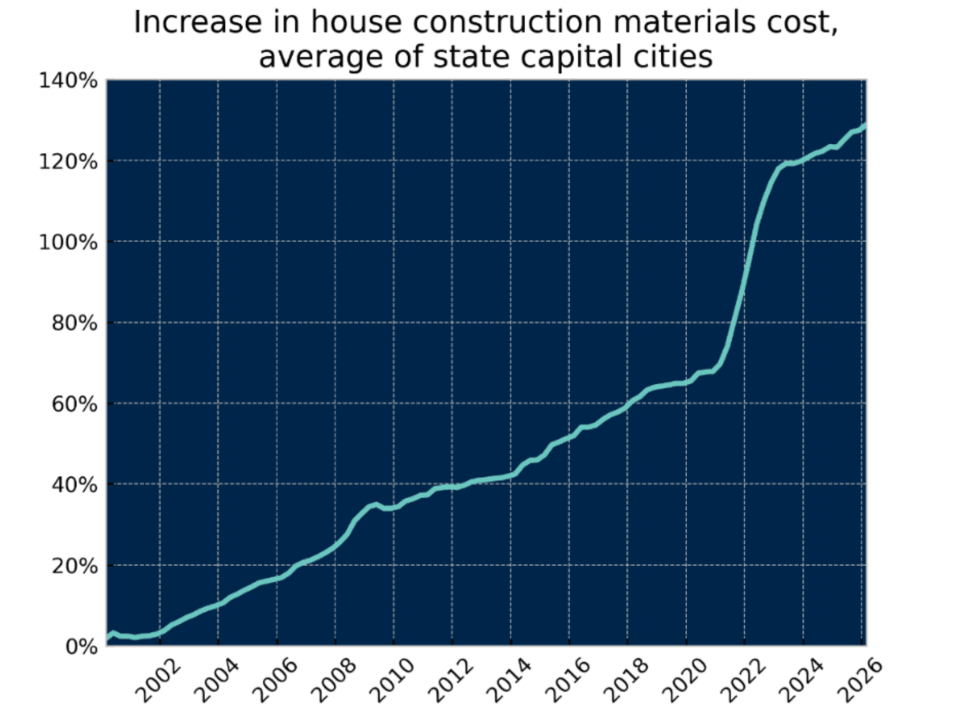

According to the ABS, average loan sizes for owner-occupier dwellings increased from $400,000 to $500,000 from 2016 to 2021 but have increased from $500,000 to $735,000 between 2021 and 2026 (more than double the increase over a similar 5-year period).

Data suggests this has something to do with the cost of materials which increased by 50% only a few years ago. The graph below shows the magnitude of this increase – and no, your eyes are not playing tricks on you – it was massive!

'Game changer' in NSW

The New South Wales government plans to partner with private companies to establish modular housing factories aimed at speeding up home construction and easing housing shortages.

The initiative will use prefabricated sections that are built off-site and assembled quickly on location.

State Planning Minister, Paul Scully, said the move would help overcome the rising cost of construction.

“There can be savings of up to 20% in time, and 50% in cost when it comes to using modern methods of construction,” Mr Scully told the ABC.

The plan focuses on medium-density housing and may involve multiple facilities across the state.

The Property Council of Australia welcomed the move, calling it a “game changer” that could deliver faster, more scalable, and sustainable housing solutions.

Developers and builders, and who could blame them, are focusing on maximising their profit margin, at a time that the cost of materials have quickly travelled north.

If you are a pensioner, living in the middle to outer suburbs with limited savings, you are not going to downsize, because there isn’t anything suitable that is affordable and no one is building anything like this.

Even those with modest wealth will baulk at paying millions for an apartment near the inner city or a new home in a cookie-cutter lifestyle village where you own the house but not the land.

Sure, there are some older retirement villages that still have lower entry costs, but these are not always attractive and come with a buyer beware warning (as NSA has consistently argued).

So, rationally, people choose by default to stay put. And who can blame them?

Leaving housing to “the market” has failed both young people and older people.

This brings us back to the aged care budget.

Aged care fail

If older people remain in larger homes that are not age friendly and require significant cost to maintain, then that raises the cost to the government.

While the government has introduced greater co-contributions for “everyday living” services, such as gardening and house cleaning, that is just pushing the cost somewhere else. It’s now the individual’s problem, but the individual doesn’t have control over the housing market.

It would be far smarter if government recognised the benefits of promoting the construction of seniors-friendly housing that is modest but attractive to the hundreds of thousands of seniors who don’t have large wealth (that’s most retirees, by the way).

The first step is understanding what older people want and then creating policies and incentives to ensure this type of housing gets built.

NSA wants older people to be part of this conversation about seniors housing.

Join our Better Housing campaign for regular updates and to have your voice heard on how we create housing that meets the needs of seniors and the wider community.

Thousands of Australia-wide discounts

Exclusive offers and savings across dining, shopping, gift cards, and more – all in the EAT | PLAY | SAVE app.

Members save 10% on Travel Insurance*

National Seniors members receive a 10% discount on travel insurance policies*.

Financial Information Consultant

Speak to a real person and receive up-to-date information on retirement planning, superannuation, and more!

Branches

Expand your social circle, enjoy social events, day trips, guest speakers, and meet like-minded members.

Exclusive Travel Discounts

Save on tours, cruises, and holidays with exclusive discounts on National Seniors Travel.

Our Generation Digital Magazine

Receive a yearly subscription to Our Generation Digital Magazine.

The Good Guys Commercial

Members enjoy exclusive access to The Good Guys Corporate Benefits. Save on small and large appliances as well as technology.

Advocacy & Research

Your membership directly funds our advocacy and research work fighting issues that affect you.

Competitions

Access exclusive member-only weekly competitions including books, DVDs, CDs, movie tickets and more.

Discounts

In addition to the discounts app, members can save thousands on eGift Cards and other discounted products.

*The discount applies to the total National Seniors travel insurance premium and is for National Seniors Australia members only. Discounts do not apply to the rate of GST and stamp duty or any changes you make to the policy. nib has the discretion to withdraw or amend this discount offer at any time. This discount cannot be used in conjunction with any other promotional offer or discount. ^ Cover is subject to terms, conditions, limitations and exclusions in the PDS.

National Seniors Australia Ltd ABN 89 050 523 003, AR 282736 is an authorised representative of nib Travel Services (Australia) Pty Ltd (nib), ABN 81 115 932 173, AFSL 308461 and act as nib's agent and not as your agent. This is general advice only. Before you buy, you should consider your needs, the Product Disclosure Statement (PDS), Financial Services Guide (FSG) and Target Market Determination (TMD) available from us. This insurance is underwritten by Pacific International Insurance Pty Ltd, ABN 83 169 311 193.