How to protect your portfolio from inflation

Inflation can quietly erode long-term returns. Paul Clitheroe shares practical ways to help protect your portfolio.

About Paul Clitheroe

Paul Clitheroe is Chairman of InvestSMART. He has been a media commentator for more than 30 years and is regarded as one of Australia's leading experts in the field of personal investment strategies and advice. Paul hosted the Channel 9 program Money, helped establish Money magazine, where he now acts as editorial adviser, and is the author of several personal finance books.

Paul is also chairman of Ecstra and the Ensemble Theatre Foundation. He is also the chair of Financial Literacy and Professor with the School of Business and Economics at Macquarie University.

Petrol prices have attracted plenty of attention lately, with some economists warning higher fuel costs could add to inflation pressures in the months ahead.

The latest available data showed inflation was 3.7% over the 12 months to February 2026. At the time of writing, Westpac and Commonwealth Bank were forecasting that inflation would peak at 5.4% over the coming months.

As investors, it is natural to be concerned about the impact of rising prices. So, let’s take a look at what you can do to protect personal wealth.

Why does inflation even matter?

“Inflation” refers to the way prices move over a given time period. In Australia, it’s measured by the Consumer Price Index (CPI).

As consumers, inflation reduces our purchasing power. For investors, inflation can be more damaging.

When prices rise, the purchasing power of our money falls. Even if your portfolio balance remains the same in dollar terms, it can be worth less in “real” (after-inflation) terms.

The higher inflation is, the harder your money has to work just to keep pace.

For example, if an investment generates a return of 5% and inflation is 4%, your “real” return is just 1% (5% less 4%).

The obvious solution is to invest in assets with higher returns. The problem is that higher returns go hand-in-hand with higher risk. And that may not suit everyone.

Fortunately, there are steps you can take that don’t involve ramping up risk.

Look for a healthy rate on savings but don't see cash as a long-term solution

In response to stubbornly high inflation, the RBA raised interest rates in March.

Investors will be watching closely to see what happens at its next meeting in May.

The upside to rising rates is better returns on many savings accounts.

Across accounts that don’t impose conditions on withdrawals and deposits, you could earn around 4.85%.

This definitely makes it worth checking the rate you’re currently earning on spare cash.

However, that doesn’t mean your whole portfolio should be sitting in cash.

Remember, your money needs to outpace inflation to retain its purchasing power. On an account earning 4.85%, with inflation running at 3.7%, you’re only earning a “real” (after inflation) return of 1.15%.

The other drawback is that returns on cash are fully taxable. A high-income earner could lose close to half their interest earnings to tax, meaning the real value of cash investments will go backwards quite quickly.

The upshot is that while it makes sense to have savings – in particular, for retirees and conservative investors – cash has historically been a wealth destroyer for investors during periods of higher inflation.

Diversify across asset classes

Diversification remains an investor’s best protection against inflation.

Different asset classes – shares, fixed interest (like bonds), commodities, and property – each behave differently in inflationary environments. Holding a mix of investments reduces the risk that inflation will erode away your entire portfolio.

Equities have historically provided strong long-term protection against inflation.

Some listed companies can pass higher costs on to consumers through price increases. Others, with strong pricing power, consistent demand and low debt, tend to be more resilient during inflationary periods.

Well located property is a classic hedge against inflation, though it requires large amounts of money. As inflation increases, you have to plan to make higher interest repayments.

For property investors, CPI-based rent increases, potential tax deductions, and the fact that inflation reduces the real size of your mortgage over time, make property an attractive inflation hedge.

Regardless of which asset class you wish to hold, exchange-traded funds (ETFs) are a great solution. They provide instant diversification with minimal effort, and ETFs span all the major asset classes.

Be mindful of costs

During inflationary times we tend to look closely at where our money is going. Now is the time to apply that same level of scrutiny to the fees you’re paying on investments.

The strength of ETFs is that many are “passively” managed. They aim to replicate the returns of a given index, and so the fees are extremely low.

In the current environment, it can be tempting to try to beat the market by investing in actively managed funds even though they typically charge higher fees.

However, the latest SPIVA Australia Scorecard confirms that in 2025, 74% of actively managed Aussie share funds failed to match market returns, while 70% of active global share funds failed to outpace the market.

Long story short, be mindful of the cost of your investments. It is fees – not returns – that are set in stone.

Don’t let inflation disrupt your commitment to investing

Many Australians are feeling the squeeze of higher living costs. As prices rise, household budgets can come under more pressure.

Where possible, though, I encourage you to keep adding to your portfolio on a regular basis.

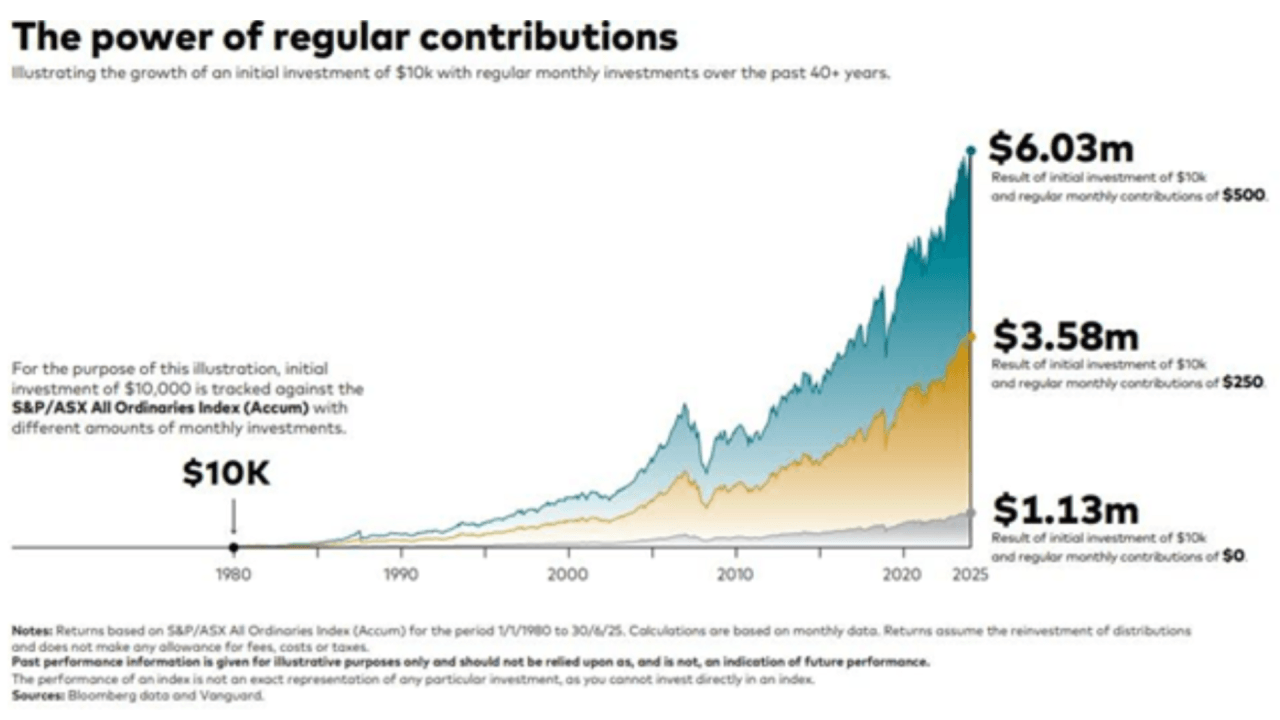

Vanguard has done some terrific research on the value of regular investing. It found that $10,000 invested in Australian shares back in 1980 would be worth $1.13 million today. If an extra $250 had been added to the same portfolio each month, it would have grown to $3.58 million. Make it $500 in monthly contributions and that same portfolio would now be worth more than $6 million.

Source: Vanguard

Stay focused on the long term

Whether it’s a crisis caused by a pandemic such as COVID, a collapse of business confidence, or an energy crisis caused by a war far away from us, the best solution for investors remains diversification.

By making spare cash work hard, diversifying across asset classes, being mindful of fees and aiming to grow your investments where you can, it’s possible to build a portfolio that is as crisis-resistant as possible – one that doesn’t just keep up with inflation, but over time stays comfortably ahead of it.

This article first appeared on InvestSMART. You can sign up to get a free newsletter, with fortnightly insights from InvestSMART’s team of experts including Paul Clitheroe and Effie Zahos.

Author Paul Clitheroe

Chairman, InvestSMART

Disclaimer: This article and any links provided are for general information only and should not be taken as constituting professional advice. National Seniors Australia is not a financial adviser. You should consider seeking independent legal, financial, taxation, or other advice to check how any information provided relates to your unique circumstances.

Thousands of Australia-wide discounts

Exclusive offers and savings across dining, shopping, gift cards, and more – all in the EAT | PLAY | SAVE app.

Members save 10% on Travel Insurance*

National Seniors members receive a 10% discount on travel insurance policies*.

Financial Information Consultant

Speak to a real person and receive up-to-date information on retirement planning, superannuation, and more!

Branches

Expand your social circle, enjoy social events, day trips, guest speakers, and meet like-minded members.

Exclusive Travel Discounts

Save on tours, cruises, and holidays with exclusive discounts on National Seniors Travel.

Our Generation Digital Magazine

Receive a yearly subscription to Our Generation Digital Magazine.

The Good Guys Commercial

Members enjoy exclusive access to The Good Guys Corporate Benefits. Save on small and large appliances as well as technology.

Advocacy & Research

Your membership directly funds our advocacy and research work fighting issues that affect you.

Competitions

Access exclusive member-only weekly competitions including books, DVDs, CDs, movie tickets and more.

Discounts

In addition to the discounts app, members can save thousands on eGift Cards and other discounted products.

*The discount applies to the total National Seniors travel insurance premium and is for National Seniors Australia members only. Discounts do not apply to the rate of GST and stamp duty or any changes you make to the policy. nib has the discretion to withdraw or amend this discount offer at any time. This discount cannot be used in conjunction with any other promotional offer or discount. ^ Cover is subject to terms, conditions, limitations and exclusions in the PDS.

National Seniors Australia Ltd ABN 89 050 523 003, AR 282736 is an authorised representative of nib Travel Services (Australia) Pty Ltd (nib), ABN 81 115 932 173, AFSL 308461 and act as nib's agent and not as your agent. This is general advice only. Before you buy, you should consider your needs, the Product Disclosure Statement (PDS), Financial Services Guide (FSG) and Target Market Determination (TMD) available from us. This insurance is underwritten by Pacific International Insurance Pty Ltd, ABN 83 169 311 193.