Inflation isn’t all bad news

Pension payments went up on 20 September, but so too did the thresholds governing eligibility to the pension and concessions cards – putting more money in your pocket.

Receiving a part pension

When your income and assets are being assessed as part of the means tests, it will be determined if you are eligible for a full pension or a part pension.

If your assets and income are above the limit for the full pension, but below the cut-off points, you may be eligible to receive the Age Pension at a reduced rate. This rate is determined by applying the results of the test – from the assets test and income test – that determines the lowest rate of pension.

In other words, if the assets test determines that your pension rate should be $100 per fortnight, and the income test determines it should be $50 per fortnight, the lower of the two is used to determine your payment rate.

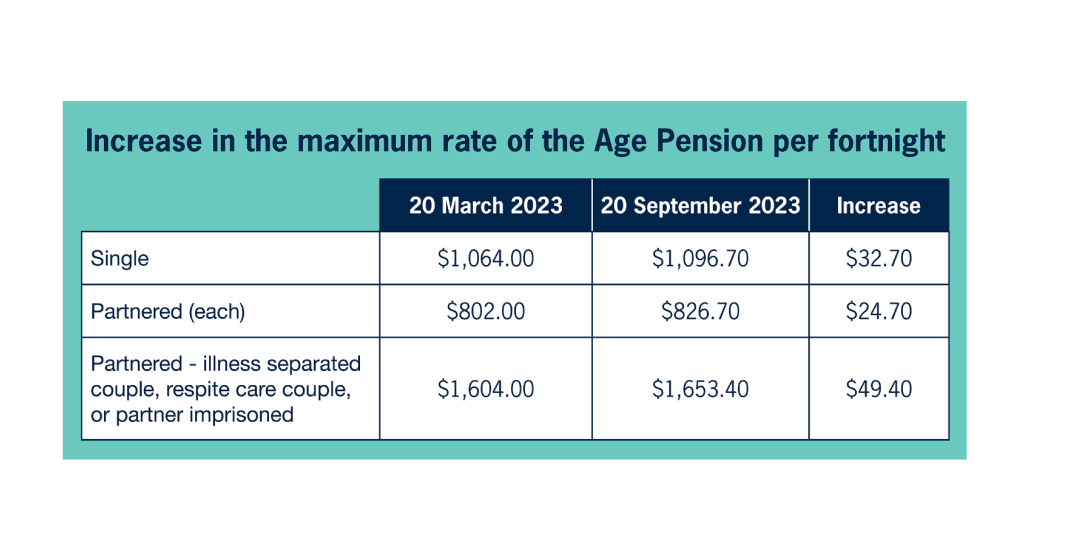

Inflation-driven cost-of-living pressures continue to bite – but they’ve also fed into the bi-annual review of pension payments and eligibility thresholds.

Some self-funded retirees who previously missed out may now be eligible for the Age Pension or Commonwealth Concession Card.

For many Age Pensioners, payments increased on 20 September in line with the twice-a-year adjustment, which considers increases in the inflation rate as measured by the Consumer Price Index (CPI).

The bi-annual review means payments always go up.

But what many people don’t realise is that CPI adjustments could also benefit self-funded retirees who previously weren’t eligible for support.

The CPI adjustment is good news. Thresholds are used to determine whether a retiree receives a part-pension, and the Pensioner Concession Card also increased on 20 September.

This means, retirees who may be just outside the Age Pension asset eligibility rules could find themselves qualifying for a part-pension.

The single, homeowner threshold will lift by $11,000. This means that a single homeowner with less than $667,500 in assets will now qualify for a part-pension.

The threshold for a home-owning couple lifts $16,500, meaning those with assets of up to $986,500 will now also qualify for a part-pension.

To find out if you’re now eligible for the pension, click here.

Being eligible for a part pension comes with a range of concessional benefits when you get a Pensioner Concession Card.

These include state and territory government pensioner concessions, designed to help retirees with cost-of-living pressures. To find out more about those concessions and to see what you qualify for, click on the National Seniors Concessions Calculator.

Commonwealth Seniors Health Card (CSHC) eligibility limits are also increasing as a result of indexation, by $5,400 to $95,400 per annum for singles and by $8,640 to $152,640 for couples combined.

With deeming rates frozen for two years, more self-funded retirees could now be eligible for concessions.

You don’t have to be a pensioner to be eligible for this card, which can save thousands of dollars in health and medical expenses.

About 40,000 more self-funded retirees have become eligible for the CSHC since the thresholds changed because of a promise to do so by both parties at the last election. More retirees will now be eligible thanks to inflation.

CSHC benefits include bigger refunds on medical costs when you reach the Medicare Safety Net, free or lower rates on other healthcare expenses (which can include ambulance transfer, eye checkups, hearing, and dental care), and, in some states, concessions on energy, water, and property rates.

Some states and territories grant CSHC holders additional concessions on the CSHC which help with cost-of-living pressures. Visit the National Seniors Concessions Calculator for more information.

Related reading: Minister’s statement, Super Guide, DSS, Age Pension Guide