Switching your super to pension phase

As a retiree, you may have more spending capacity than you think.

National Seniors Australia members receive a 19% discount on Bec Wilson's bestselling book, How to Have an Epic Retirement. Claim your discount now!

There’s a peculiar situation in Australia right now. We have 4.1 million retirees according to the latest Census, but only 1.3 million people have shifted their superannuation into the retirement phase and started drawing down on it. The rest are holding onto it in the accumulation phase, and this raises a simple question: why?

While some of these people holding back on shifting their funds are no doubt doing so strategically, in most cases, I suspect many people with smaller superannuation balances simply don’t understand how their fund works. And many people are unfamiliar with the differences between accumulation phase and retirement phase superannuation fund earnings and tax.

Retirement phase superannuation performance doesn’t feature very often in the media, and there is a real lack of benchmarking for retirement phase superannuation funds available to consumers. So there’s not many places that people can learn about it either, particularly if they aren’t regularly engaging with their superannuation fund.

It's important for everyone approaching the retirement phase, and those already in it, to better understand how it works. So, today I’m taking a brief look at the retirement phase of superannuation, how it works, and comparing the performance of Australia's major fund managers' retirement phase funds to their accumulation phase funds.

But first, let’s clarify the core differences between the accumulation phase and the retirement phase.

The accumulation phase is the early stage of superannuation where people contribute money to their superannuation fund to build their retirement savings.

During this phase, we contribute funds into our superannuation account, aiming to accumulate wealth through the combination of savings and compound investing.

The investment focus in the accumulation phase is typically on long-term growth and capital accumulation, with a portfolio usually incorporating some higher-risk assets such as stocks and growth-oriented investments.

Investment earnings within the superannuation fund are taxed at a concessional rate of 15% during the accumulation phase. During the accumulation phase, people can usually only access their superannuation if they reach preservation age or meet the conditions of release which would see it shifted into retirement phase or withdrawn.

The retirement phase, which is also known as the pension phase or drawdown phase, kicks off when a person turns 60 and meets the conditions of release and transfers their fund into this phase.

Retirees in this phase can draw an income stream from their superannuation fund or withdraw their funds as a lump sum.

The investment approach often adjusts upon retirement to accommodate any changes in risk tolerance as individuals now rely on their superannuation for income. Once in the retirement phase, individuals must meet the minimum annual drawdown amounts, starting at 4% for those aged 60-65 years, increasing with age.

The objective of the compulsory drawdown is to encourage retirees to utilise their savings in superannuation to fund their retirement lifestyle and cost of living.

It’s important to note that accumulation phase funds are taxed at 15%. However, once an individual reaches the age of 60, all investment earnings and pension payments in the retirement phase are tax-free, unless your balance exceeds the transfer balance cap or the proposed $3million cap under new legislation. This tax-free status significantly enhances the tax efficiency of the retirement phase for retirees.

As I mentioned earlier, retirement phase superannuation funds usually outperform the accumulation fund with a similar investment mix, mainly because retirees don’t pay capital gains tax (CGT) or income tax unless their assets are over the transfer balance cap.

These tax benefits, combined with the appropriate investment mix, and careful management, often lead to better net returns for retirees in the pension phase compared to those in the accumulation phase with similar investment portfolios.

But retirement phase funds are not publicly benchmarked, so it is difficult to compare them.

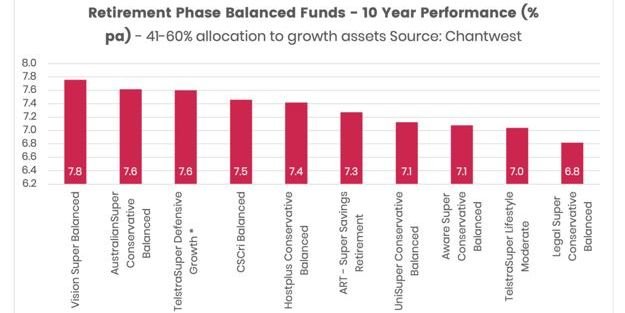

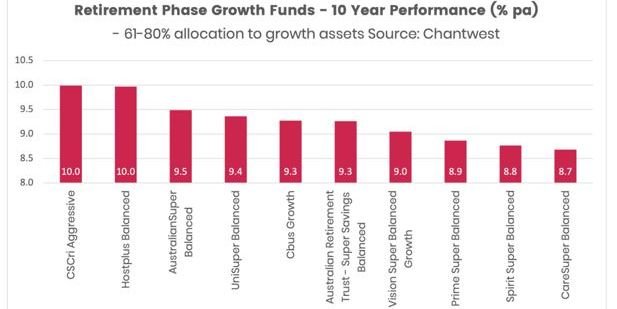

So, I’ve sourced for you a snapshot of the top 10 balanced retirement phase superannuation funds over the last 10 years and the top 10 growth retirement phase superannuation funds over the last 10 years, both to June 2023.

Consider that over the last 10 years, the top 10 balanced funds in accumulation phase Australia achieved returns between 6.1% and 6.9%.

And the top 10 growth funds in accumulation phase achieved returns of between 7.98% and 8.93%.

To give you a more direct comparison against accumulation funds, I’ve done a deep dive into three of Australia’s largest funds to compare accumulation and pension fund returns.

Telstra Super Growth has performed over a 10-year period at 7.99% in accumulation and their Lifestyle Growth fund has performed at 8.84% return in the retirement phase.

REST’s Diversified Accumulation fund has delivered a 7.58% return in accumulation and 8.31% in pension phase over 10 years.

Australian Super’s Balanced Fund had a 10-year return of 8.6% in accumulation and 9.48% in pension phase.

In all three cases, the retirement phase products outperformed their accumulation phase counterparts.

And, knowing why, you might also want to consider if that gives you a little more confidence in your retirement income. Most people, when they first start to draw a retirement income stream, are nervous about running out of money, and they therefore tick the 'minimum drawdown’ box on their account-based pension, more out of fear than good reason.

Nerves shouldn’t drive this decision. In fact, it really is crucial to pause and reflect on whether you can afford to draw more to enhance your retirement experience. Many people live cautiously in their retirement years, fearing the unknown and, consequently, accumulate more wealth than they anticipated, having lived too frugally.

Would you do it differently if you better understood your superannuation? It could be worthwhile taking a moment to contemplate this and seeking guidance from a financial adviser or your super fund so you can see the bigger picture and potentially set yourself up for a more epic retirement.